Main Highlights

Top Three Sports Bars in Arlington, Virginia: Crystal City Sports Pub, First Down Sports Bar and Dudley’s Sport and Ale

Recall of 43,000 Pounds of Ground Beef over E. Coli Concerns: What You Need to Know

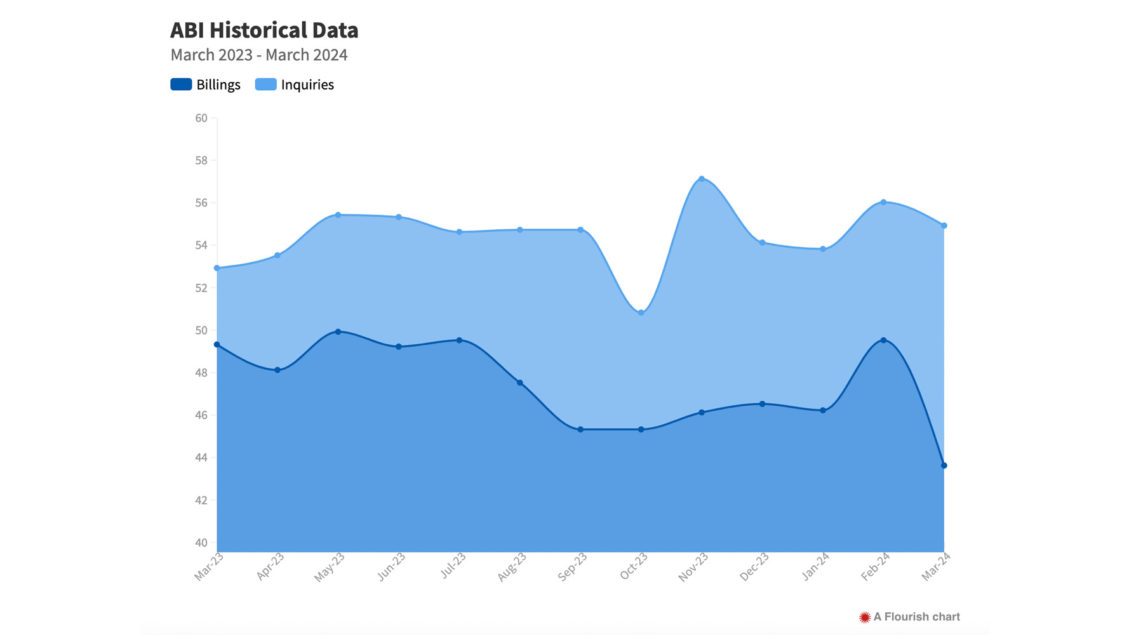

Despite Challenges, Institutional Design Shows Signs of Stability: AIA/Deltek Architecture Billings Index Recorded at 43.6 in March